A sweeping overhaul of bank capital rules proposed by regulators includes changes to requirements for residential mortgages that will likely inflame criticism that the measures push home-ownership beyond the reach of first-time or minority borrowers.

The long-awaited proposals would raise the so-called risk weights for some residential mortgages, including those with smaller down payments, meaning banks ultimately have to hold more capital against those assets.

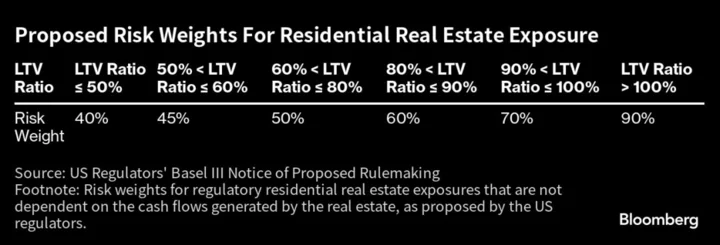

Currently in the US, a 50% risk weight is assigned to many first-lien residential mortgage loans. Under the new proposals, regulators would apply risk weights of 40% to 90% for large banks, depending on the loan-to-value ratio. Riskier loans, with higher LTV ratios, would get the higher risk weights.

Critics have warned the reforms could exacerbate a pull-back by banks from lending to riskier borrowers with less money to put down, or shut them out completely as borrowing costs rise as a consequence. The adjustments go beyond international standards — the Basel III framework — by about 20 percentage points.

Read more: US Banks Face Stiffer Mortgage Capital Rule Than Global Standard

“Banks should not use higher capital requirements as an excuse to reduce lending to low income or first time borrowers,” said Mayra Rodriguez Valladares, a financial risk consultant at MRV Associates, who previously worked at the New York Fed. “If banks sell some of their securitizations, longer-term derivatives, or alternative investments such as property, that reduces their risk and improves their capital ratios. This means that they would be able to lend comfortably to a wide range of borrowers.”

The Mortgage Bankers Association, along with other industry groups, signed a letter to regulators this week warning the capital standards will have a “devastating impact” on efforts to increase Black homeownership as well as disadvantaging first-time homebuyers. A LendingTree study published this week found that the denial rate for Black homebuyers across the 50 largest US metro areas is on average 5.3% higher than the denial rate among overall mortgage borrowers.

Read more: Biggest Banks Face 19% Boost in Capital Requirements in US Plan

The revamp of the rules, which would force lenders to bolster their financial cushions to absorb losses, are part of a review that Michael Barr began as one of his first acts as the Federal Reserve’s vice chairman for supervision. In a statement Thursday, Barr said capital requirements are crucial to financial stability, as he invited institutions to comment on the proposals.

“The proposal does adjust the size thresholds for capital rules, and we will benefit from additional views on whether the benefits of that increased resiliency outweigh the costs,” he said. “We want to ensure that the proposal does not unduly affect mortgage lending, including mortgages to under-served borrowers.”

Regulators are aware that the proposed changes could hurt borrowers who are only able to afford small down payments on their home, agency officials said Thursday. That’s why they’re requesting feedback on whether they should apply one standard risk weight against mortgages rather than a range.

Jonathan McKernan, a Republican board member at the Federal Deposit Insurance Corporation, warned in his dissent to the proposal that “there likely will be real economic costs” to the agencies move on mortgages.

“Large banks generally would see an increase in the capital requirement on mortgage loans to borrowers who cannot afford a 20% down payment,” he said. “The increased capital requirements could lead to an increase in interest rates for low- and moderate-income and other historically underserved borrowers who cannot always afford a 20% down payment, making it that much harder for these families to achieve homeownership.”

Everyday Americans

While regulators argue the more conservative approach benefits the financial system overall, some banking executives criticize certain elements. JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon has said that higher capital requirements mean it “barely makes sense for banks to hold mortgages or mortgage-servicing rights,” a situation that “ultimately hurts everyday Americans.”

The reforms also come amid a protracted retreat by banks from originating home loans, a business they dominated heading into 2008 financial crisis. After the bust, many large lenders faced tens of billions of dollars in liability from mortgage-related operations and retrenched, ceding the top spots to a new breed of online mortgage lenders like Rocket Companies Inc.

JPMorgan and Wells Fargo & Co.’s origination volume fell from 2012 to 2021, even as the overall industry’s total more than doubled. Both banks have dismissed swaths of employees over the past months as soaring interest rates quelled demand for homes.

“Without significant revisions, this proposal will increase borrowing costs and reduce credit availability for the very consumers and borrowers this administration ostensibly seeks to assist,” Bob Broeksmit, president of the MBA, said in a statement. “Given ongoing affordable housing challenges, regulators should be taking steps that encourage banks to better support real estate finance markets. These proposed changes do precisely the opposite.”

--With assistance from Stephanie Stoughton.

(Updates with FDIC board member comment in tenth paragraph. An earlier version of the story corrected the date of the regulator’s statement.)