Tucked away in hours of congressional testimony by Federal Reserve Chair Jerome Powell last month was an admission that the central bank was blindsided by the impact of shrinking its balance sheet four years ago.

While Powell assured lawmakers the Fed is committed to avoiding a repeat of 2019 — when the repo market, a key part of US financial plumbing, seized up — Wall Street economists and strategists caution that quantitative tightening remains complex and hard to predict. Known as QT, it involves letting Fed bond holdings mature without replacement, draining cash from the financial system.

In the coming months, the full brunt of the Fed’s current QT program is set to be felt. How it proceeds, and how the Fed handles the process, could shape its political latitude to keep using its balance sheet as a key tool in the future, amid Republican angst that was on display in Powell’s June 21-22 hearings.

“We didn’t see it coming,” Powell acknowledged at the House Financial Services Committee June 21 when referencing the sudden problems that emerged in 2019 and forced the central bank into steps it didn’t want. The advantage now is “we have experience,” he said.

The Fed is currently shedding its bond holdings at an annual pace of roughly $1 trillion, much faster than in 2019 but from a much bigger base. Powell told lawmakers he’s “very conscious” of the importance of not just inflating the balance sheet during each easing cycle and leaving it enlarged.

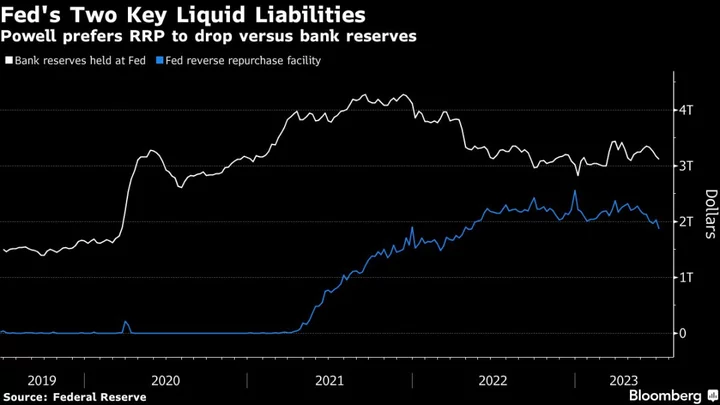

So far, Powell and market participants agree, things have been going smoothly. There are still more than $3.2 trillion of bank reserves parked at the Fed, and no indication that that gauge of liquidity has shrunk to a level that would cause problems in money markets as happened in 2019. Analysts estimate — with low conviction — the banking system needs at least $2.5 trillion to function smoothly.

“You don’t want to find yourself, as we did a few years back, suddenly finding that reserves were scarce,” Powell said last month. This time, the goal is to slow QT down at some point, ending the bond-portfolio runoff when reserves are still “abundant,” with an added buffer “so we don’t accidentally run into reserve scarcity.”

One reason things are going well so far is that there’s another big element of liquidity on the Fed’s balance sheet — the reverse repo facility. Known as RRP, money-market funds have used it to park cash. And that account stands at more than $1.8 trillion.

Full Impact

Another reason is that the overall Fed balance sheet has only shrunk by a fraction of the amount it surged during the pandemic. The Fed’s liquidity injections during the spring — to help address regional bank troubles — expanded the balance sheet. The Treasury was also limiting sales of bills — which remove liquidity — while it was constrained by the debt-limit standoff.

Those two dynamics have largely ended now, however.

“Things will start tightening on the liquidity side,” predicted Raghuram Rajan, the former International Monetary Fund chief economist and Indian central bank governor. “Then we will see the full consequences” of QT, the University of Chicago economist said last week on Bloomberg Television.

Even then, a number of observers see things going relatively smoothly. That’s because QT could end up mainly draining RRP. Indeed, it’s already receded to the lowest level since May 2022.

Powell’s Preference

The RRP can shrink “dramatically” without “particularly important macroeconomic effects,” Powell explained last month. And he told a Senate panel that “that’s what we would have hoped to see, rather than taking reserves out of the system.”

With the Treasury in the middle of ramping up its own cash reserve by as much as $1 trillion, market participants will be closely monitoring what gets drained as that goes ahead.

Bank of America Corp. strategists, led by Mark Cabana, estimate that 90% of the Treasury’s issuance will be funded by the RRP, as money-market funds shift from that Fed facility to investing in higher-yielding T-bills.

Others aren’t so sure.

Others’ Doubts

RBC Capital Markets analysis indicates that, so far, about 60% of the Treasury’s sales are coming from draining the RRP. Even that pace is faster than Blake Gwinn and Izaac Brook expected, and those strategists see the rate slipping to 45% to 50%. If households and companies keep pouring cash into money-market funds, they say, that could leave them still needing to park large amounts in the RRP, slowing its decline.

Read More: Money Markets Are Giving Fed Room to Keep Shedding Treasuries

Gennadiy Goldberg, head of US rates strategy at TD Securities Inc., said it’s unclear how the Treasury’s bill sales will be funded. And that in turn leaves the impact of the Fed’s QT a question mark.

“Saying everything is OK is like calling the game after the first quarter,” he said. “Last time the Fed hit the wall at 60 miles an hour as they weren’t expecting reserve scarcity to be there — and the risk now again bears watching.”

There are other potential issues, to boot.

Dina Marchioni, director of money markets at the New York Fed, said at a symposium last month that staff are watching for the potential to money-market funds to start buying slightly longer-dated assets — something they might do to lock in yields for longer as the Fed approaches the end of interest-rate hikes.

Tools Available

That could put upward pressure on very short-term rates, sending them above the Fed’s target rate, Marchioni indicated.

The central bank does have policy tools it can use to address challenges, including a standing repo facility that offers cash overnight in exchange for securities, and the recently established Bank Term Funding Program.

“The risk scenario is that they do too much, too fast and then disrupt the flow of credit to the economy by so much that it tips things over to recession,” said Seth Carpenter, a former Treasury official who is now global chief economist at Morgan Stanley. But “that is not at all our base case,” he added, expecting QT to last well into next year.

Still, even Fed staff — as revealed in minutes of the most recent policy meeting — last month viewed with “uncertainty” their expectation for bank reserves to remain “abundant” by year-end.

“The biggest unknown at the moment is what is the lowest comfortable level of reserves in the financial system,” said TD’s Goldberg. “We just don’t know.”

Author: Liz Capo McCormick, Alexandra Harris and Jonnelle Marte