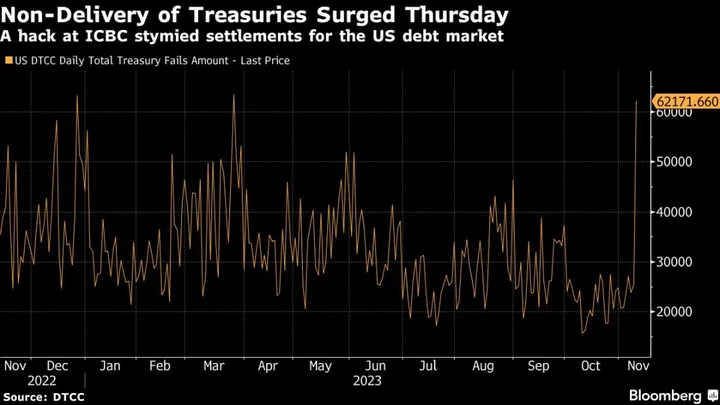

Non-delivery of US debt pledged as collateral surged on Thursday as the repercussions of a cyberattack on Industrial & Commercial Bank of China Ltd. rippled through the market.

US Treasury repo fails — the amount of US debt that wasn’t delivered to fulfill trade contracts — rose to $62.2 billion, the highest since March and up from $25.5 billion a day earlier, Depository Trust & Clearing Corporation data show. Such failures-to-deliver occur when either sellers do not deliver, or buyers do not receive, securities in time to settle a trade.

The repo market — which usually closes at 3 p.m. in New York — stayed open until 7 p.m. in order to facilitate trades, according to Subadra Rajappa, head of US interest-rates strategy at Societe Generale. And the Federal Reserve kept its Fedwire settlement system open to minimize the damage, said Curvature Securities executive vice president Scott Skyrm.

The DTCC and Fed could not immediately be reached for comment on the extensions.

“We saw our fails increase by maybe 50% or doubled,” said Skyrm. “We would’ve had a lot more fails if they hadn’t stayed open. That cleaned up some of the fails and helped the congestion,” he said.

Rumors around the attack on ICBC swirled through markets on Thursday as entities responsible for settling transactions swiftly disconnected their systems to contain the damage, forcing ICBC to send settlement details via a USB drive. The drama complicated the US’s auction of 30-year debt, which was among the worst in a decade, with some market participants citing ICBC’s troubles as adding to the lackluster result.