A pickup in losses in China bonds has sent local money managers rushing to reassure jittery clients that there won’t be a repetition of last year’s record withdrawals.

The nation’s biggest lender, Industrial & Commercial Bank of China Ltd. told its private bank clients in a statement Monday that a sharp pullback in the bond market is unlikely, mirroring commentary from peers like Industrial Bank Co. and HSBC Jintrust Fund. ICBC’s argument was that it’s too early to call an end to monetary easing and give up on bonds, given the slow recovery in the world’s second largest economy.

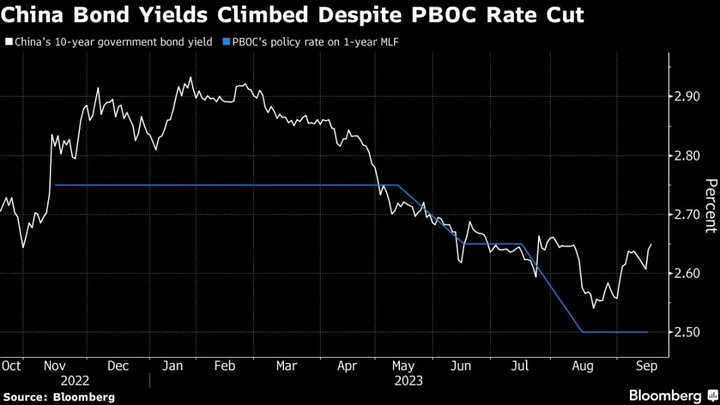

A Bloomberg index of China’s bonds is on track for its first monthly loss since November, as risk sentiment improves and traders become less convinced the central bank will cut interest rates swiftly when authorities are rolling out other measures to stimulate the ailing property market. The abrupt reversal of what had been a strong bond rally this year resembles the early stage of the debt market turmoil during Beijing’s Covid policy pivot late last year.

Back then, China’s retail investors sold out of fixed-income investments to limit losses when bond yields suddenly jumped, fueling a record exodus by mutual funds and wealth management products. Regulators had to rush to steady the market by urging lenders and insurers to buy the securities.

Since late August, China’s benchmark 10-year yield has climbed over 10 basis points having slumped to its lowest in more than three years — thanks to nascent signs of stabilization in the economy. The Bloomberg bond index has fallen 0.4% so far this month in local currency terms — its 1% slump in November was the worst since 2020.

“We think the chances for a large decline in bonds are low and there is still a relatively high allocation in bond funds,” said Cai Ruolin, a bond fund manager at HSBC Jintrust Fund Management Co. “There is still downward pressure for China’s macro economy and policy makers will strike a balance between stabilizing the economy and preventing risks.”

China’s latest economic figures are mixed — new loans, industrial production and retail sales data are improving while a decline in home prices accelerated in August. China will step up policy adjustment to reach annual growth target, Cong Liang, Vice Chairman of the National Development and Reform Commission said at a presser on Wednesday.

Chinese banks decided to keep the benchmark lending rates unchanged Wednesday morning, tracking the steady policy rate in the central bank’s liquidity operation for this month.

Feedback Loop

The pushback by China’s money managers highlights efforts to head off another negative feedback loop for their products at the very time when investors are considering their asset allocation. Bonds accounted for 16.2 trillion yuan ($2.2 trillion) of assets in wealth management products issued by banks, a share of 58%, according to official data from the end of June. The market is dominated by individual investors.

Just 4% of wealth management products dropped below their net asset values in September, compared to more than 20% last year, ICBC said in its statement. Industrial Bank also sought to soothe client nerves in a webcast Monday, suggesting China’s latest bank reserve requirement cut reinforced a dovish stance that will help the bond market stabilize.

“The RRR cut shows the PBOC is aware of market volatility and wishes to stabilize the funding condition of banks,” Pang Bo, a fixed-income investment manager at the bank’s wealth management unit said in the webcast. “Broadly, the bond market may not see a reversal too soon, not before economic momentum shifts fundamentally.”

--With assistance from Jonas Bergman.

(Updates with official comments on the economy and loan prime rate decision in the 7th and 8th paragraphs)