Asian shares advanced while Treasuries jumped following dovish comments on rates from Federal Reserve officials.

Stocks in Australia, Japan and South Korea all rose by more than 1%. Futures in Hong Kong also pointed to gains. Contracts of US stocks were little changed in early hours in Asia after the S&P 500 advanced 0.6% Monday.

Treasuries jumped at the open as trading resumed following a holiday, with yields on the benchmark 10-year dropping 15 basis points to 4.65% Tuesday. Yields on Australian and New Zealand bonds also declined.

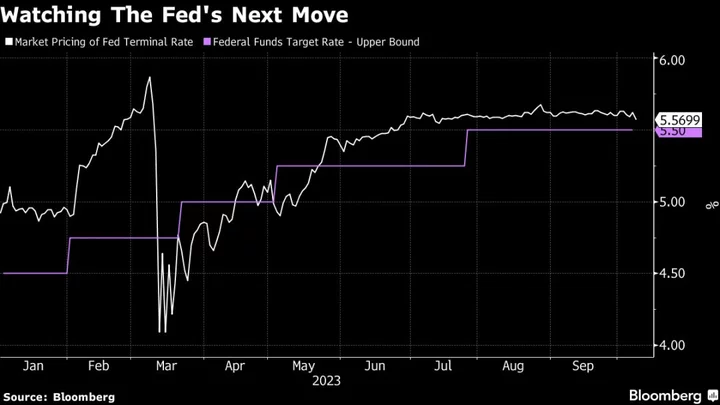

Fed Vice Chair Philip Jefferson said officials could “proceed carefully” following the recent rise in Treasury yields, and Fed Bank of Dallas President Lorie Logan said the surge in long-term rates may mean less need for further tightening.

At the end of last week, traders had boosted bets on another Fed hike this year as data showed US employment unexpectedly surged in September. That narrative was switched on Monday as central bank officials damped down speculation of another rate increase in 2023.

“The script has changed,” said Andrew Brenner at NatAlliance Securities. “The odds for another tightening have dropped dramatically since Friday.”

Read: Wall Street’s Narrative Gets Lost in World of Hurt: Surveillance

West Texas Intermediate retreated slightly after previous gains as Hamas’ attack on Israel raised fears of a wider conflict that could constrain energy supplies. Gold extended its climb into a third day after its biggest one-day gain since May on haven buying Monday in the wake of the fighting. The dollar edged lower.

No Quick Fix

In Asia, data Monday showed China’s daily new-home sales during the eight-day Golden Week holiday declined 17% from last year, showing there’s no quick fix for a record housing-market slump that’s stifling economic growth and worsening a debt crisis among developers.

Energy companies led gains Monday in the S&P 500 as US crude futures briefly topped $87 a barrel. Exxon Mobil Corp. and Chevron Corp. added over 2.7%. Defense companies rallied, with Northrop Grumman Corp. up the most since March 2020 and Lockheed Martin Corp. gaining 8.9%. American Airlines Group Inc. and Delta Air Lines Inc. fell more than 4%.

Israel’s shekel dropped even after the central bank unveiled a $45 billion support program. Gas prices in Europe soared.

Read: Five Key Charts to Watch in Global Commodities This Week

The latest Middle East conflict comes at a time of ongoing geopolitical concerns, with markets also facing a period of moderating global economic growth, according to Solita Marcelli, chief investment officer Americas at UBS Global Wealth Management

“Against this backdrop, we continue to prefer fixed income to equities,” Marcelli noted. “We see a better risk-reward profile for fixed income, and we recommend investors consider buying high-quality bonds in the 5-10-year maturity range. We foresee further cooling in inflation and slower global growth.”

The next risk to US stocks could come from fiscal policy constraints at a time when the Fed is still fighting high inflation, according to Morgan Stanley’s Michael Wilson. The strategist — among the most prominent bearish voices on Wall Street — said while the US government narrowly avoided a shutdown last week, “the lack of a resilient long-term structure that supports fiscal discipline” could have an impact on financial markets.

Read: JPMorgan, Citi Gird For Recession Risk: US Earnings Week Ahead

Key events this week:

- Bank of England releases minutes of financial policy meeting, Tuesday

- IMF issues its latest world economic outlook, Tuesday

- US wholesale inventories, Tuesday

- Fed’s Raphael Bostic, Christopher Waller, Neel Kashkari and Mary Daly speak at separate events, Tuesday

- Germany CPI, Wednesday

- NATO defense ministers meeting in Brussels, Wednesday

- Russia Energy Week in Moscow, with officials from OPEC members and others, Wednesday

- US PPI, Wednesday

- Minutes of Fed’s September policy meeting, Wednesday

- Fed’s Michelle Bowman and Raphael Bostic speak at separate events, Wednesday

- Japan machinery orders, PPI, Thursday

- Bank of Japan’s Asahi Noguchi speaks, Thursday

- UK industrial production, Thursday

- US initial jobless claims, CPI, Thursday

- European Central Bank publishes account of September policy meeting, Thursday

- Fed’s Raphael Bostic speaks, Thursday

- China CPI, PPI, trade, Friday

- Eurozone industrial production, Friday

- US University of Michigan consumer sentiment, Friday

- Citigroup, JPMorgan, Wells Fargo, BlackRock results as the quarterly earnings season kicks off, Friday

- G20 finance ministers and central bankers meet as part of IMF gathering, Friday

- ECB President Christine Lagarde, IMF Managing Director Kristalina Georgieva speak on IMF panel, Friday

- Fed’s Patrick Harker speaks, Friday

Some of the main moves in markets:

Stocks

- S&P 500 futures were little changed as of 9:29 a.m Tokyo time. The S&P 500 rose 0.6% on Monday

- Nasdaq 100 futures were little changed. The Nasdaq 100 rose 0.5%

- Hang Seng futures rose 0.5%

- Japan’s Topix rose 1.9%

- Australia’s S&P/ASX 200 rose 1.1%

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro was little changed at $1.0577

- The Japanese yen was little changed at 148.48 per dollar

- The offshore yuan was little changed at 7.2875 per dollar

- The Australian dollar rose 0.2% to $0.6422

Cryptocurrencies

- Bitcoin rose 0.2% to $27,619.37

- Ether rose 0.3% to $1,582.13

Bonds

- The yield on 10-year Treasuries declined 15 basis points to 4.65%

- Australia’s 10-year yield declined nine basis points to 4.43%

Commodities

- West Texas Intermediate crude fell 0.3% to $86.16 a barrel

- Spot gold was little changed

This story was produced with the assistance of Bloomberg Automation.